The reason why profits are high

Monopolies? Oligopolies? No, something else.

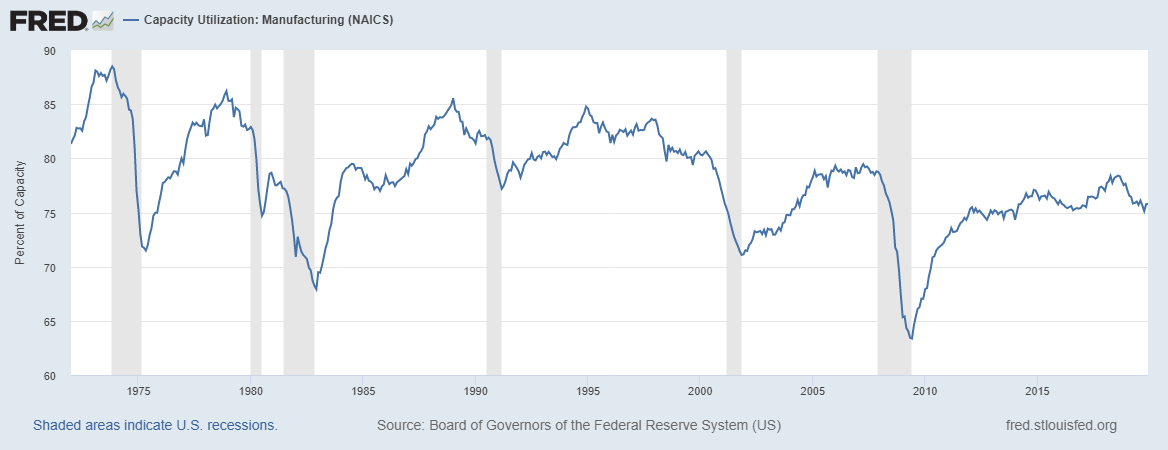

Another mystery. And another divergence. This time it's the fall in capacity utilization in the manufacturing sector. Utilization in the U.S fell from about 83% in the late '90s to 76% in 2019.

Outside the U.S, utilization has seen no downtrend post-2000.

What has caused the drop in U.S utilization? Has demand for manufactured goods fallen since 2000, leaving manufacturers high and dry? No. Manufacturing output was higher in 2019 than in 2000.

It must then be a case of manufacturers adding too much supply. But why add capacity if there is no demand for it?

Consider what happens when additional firms enter a particular market segment. These new entrants will steal market share away from the incumbents. The incumbent firms' sales will fall and they will be forced to cut output, resulting in them having an excess of capacity.

This still leaves the question of why are all these firms entering these markets and why is this only happening in the U.S? If this was happening everywhere one might be tempted to say that the internet has reduced the cost of entry (marketing and distribution costs might have fallen, for example) and led to more competition. The fact that a higher rate of entry has only taken place in the U.S, rules that out.

Let's come at this from a different angle. What economic scenarios can give rise to too many firms entering a market segment. There are two. The first is if firms are willing to make less profitable returns when they enter a new market. This would require a fall in the cost of capital. Now the cost of capital has fallen, but as my previous post explained, firms are not taking advantage of this lower cost of capital. Instead, they still want to make the returns on capital they have enjoyed historically.

The second reason why firms would be keen to jump into a new market segment is if the incumbent firms became more profitable. With a bigger pot of money to go around, a smaller market share suffices for firms to make their desired return on capital.

If workers' wages come under pressure, then firms will see rising profits. And, it is the case that corporations are now more profitable; the labor share of income has fallen in the U.S since 2000.

Outside the U.S though the labor share of income has remained pretty stable.

Therefore we can be quite confident in attributing the rise in U.S manufacturing excess capacity to the fall in the U.S labor share.

Not just manufacturing

Excess capacity has risen in the manufacturing sector, but what about services? The same logic regarding firms entering sectors to compete away higher returns should apply there too. There is no capacity utilization data series for services as a whole, but for particular sectors, we do also see falling utilization.

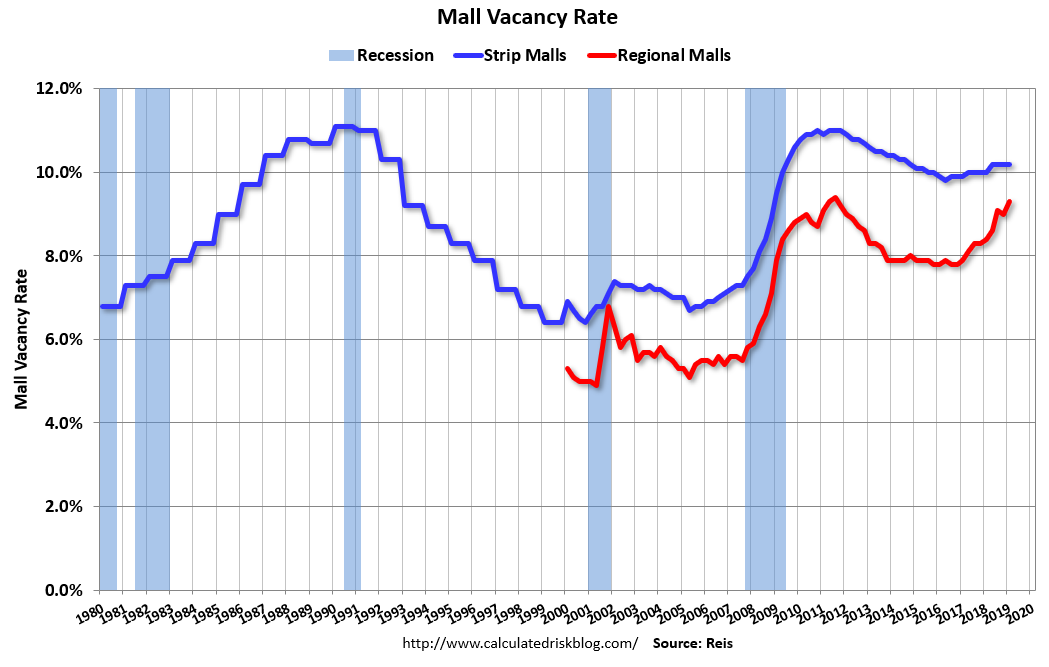

Here is a chart of the occupancy rate for office buildings, from calculatedriskblog.com

The vacancy rate surged in the '80s because of the huge construction boom that took place during the Savings and Loans bubble but had dropped back to normal levels by 2000. The subsequent increase took the vacancy rate from 8% in 2000 to 17% in 2019. This is very similar to the increase in excess capacity in the manufacturing sector.

A similar tale can be told for shopping malls:

There is a smaller increase in the vacancy rate, but I suspect that is a measurement issue. When a shopping mall has a lot of vacant leases, it likely stops trying to market the empty stores and so falls out of the survey.

In a previous post, I promised to explain the connection between the fall in the labor share and the increase in effort. How do higher effort levels push wages down? This is really quite straightforward. In response to higher effort levels, workers try and drop down to lower-skilled job positions (or refuse to move up to more senior roles). But there aren't enough job positions for all workers to drop down to, thus competition for jobs becomes fiercer. Employers are well aware that there are many applicants for each job and can afford to only give modest pay rises, pay rises that lag the increase in labor productivity. The result is a fall in the labor share of income.

The fall in labor share is not dramatic; it is still within the post-war range and higher than it was in the 50s and 60s.

Many commentators don't see anything abnormal about the post-2000 drop in the labor share for this reason. Instead, they may well view the 70s, 80's and 90's as a period in which the labor share was unusually high and the post-2000 period as a return to a more normal level of profitability. Obviously, the fact that profits have only risen in the U.S undermines that narrative. Still, why did the post-war era have a higher profit share?

I think that the explanation put forward by many economists to explain the current high level of profits In the U.S - more oligopolies and monopolies - was much more true of the post-war era. Back in the '60s, IBM for example, was the computing equivalent of Apple, Microsoft, and Google all rolled into one. The Big Three Automakers: Ford, GM, and Chrysler had an 85% market share in the '60s whilst in 2019 the combined market share was less than 50%. Other dominant companies included AT&T, Xerox, and Eastman Kodak.

The decline in profitability that started in the '70s coincided with foreign firms entering a range of markets: cars, cameras, household goods, etc. The internet should have allowed this trend to continue post-2000, the competitive landscape thus becomes flatter, and therefore profits would have declined even further, but for the rise in effort and job search costs.

You'll notice that the increase in capacity in manufacturing and vacancy in real estate is not equal to the increase in profits.

The increase in manufacturing capacity1 and office vacancy is about 8% but the increase in profits is around 12%. This is because there are barriers to entry. In manufacturing and services, these barriers are technological, scale, regulatory, and so on. For office leasing companies, the barriers are zoning (can't build in Central Park) and physical - if your city is hemmed in by mountains or water, you can only build upwards and that requires demolishing an existing building first.

Jason Furman and Peter Orszag published a paper back in 2015 that looked at the returns on capital firms were earning from 2000 to 2014. What they showed was that returns had increased but not equally; instead, there was a greater variance in returns as well.

If a sector has high enough barriers to entry then no new firms will arrive to compete away profits. These sectors tend to either be dominated by one firm - a monopoly or by a handful of firms - an oligopoly. These sectors will see an increase in profits, no fall in capacity utilization, and an increase in returns on capital. Firms that are monopolists or are part of an oligopoly are likely to be earning high returns on capital in the first place and thus the effect of falling wages is for these firms to earn still higher returns on capital.

Sympathy for the devil

Businesses must feel bewildered by all this talk of more monopolies and growing market power. From their point of view, business is unusually competitive with firms willing to jump into new market segments without having a particularly impressive new product or cost advantage.

For whatever reason, firms themselves don’t seem to be making the connection between higher profits and falling capacity utilization. Nor have I read anything in either the business press or from economists on the subject.

I’ll finish by noting that you don’t have to believe that higher effort levels are driving down wages and the labor share. If some other force2 is pushing down wages - declining union membership reducing the bargaining power of workers for instance3, then this would also lead to a higher number of firms entering markets and greater excess capacity and occupancy.

Capacity utilization in 2000 was only 80% but utilization fell sharply in the late '90s due to the East Asian crisis that reduced demand for American exports and pushed up the value of the dollar.

Excluding greater market power or biased technological change.